The considerations are different for high-net-wealth clients and aged care. With less focus on Centrelink and reducing fees and a greater focus on cash flow structuring and estate planning. It is worth understanding the best planning tips and the major pitfalls.

High net wealth clients and aged care – background

The transition to an aged care residence is often emotional and stressful. This time is where appropriate financial and legal advice can give clients confidence and content that the right decisions are made. There are many fee scenarios in which people entering aged care can be experiencing.

One of the critical financial concerns with moving to an aged care home for those of high net wealth (HNW) is the most beneficial cash flow and estate planning structure. Still, there are fundamental strategies that financial and legal advisers can use with their clients to maximise cash flow.

Pay via Refundable Accommodation Deposit, Daily Accommodation Payment, or a combination of both

In many cases, the highest cost with transitioning into an aged care home is the accommodation fee, frequently requiring the sale of assets, including the family home.

There are mechanisms in place for those with little means to have their accommodation subsidised by the Government. However, many will need to pay the accommodation payment published by their chosen aged care home. Or pay a lower amount agreed with the home.

The resident has three options to pay their accommodation payment amount. First, they can pay the amount as:

- A lump sum:

A lump sum is a refundable accommodation amount. There are two types of lump-sum payments, depending on the result of your means assessment:

- Refundable accommodation contribution (RAC): the Government assists with the costs.

- Refundable accommodation deposit (RAD): you pay the total amount yourself.

- Rental-style daily payments:

These payments are a daily accommodation fee. There are two types of daily rental payments, depending on the result of your means assessment:

- Daily accommodation contribution (DAC): the Government assists with the costs.

- Daily accommodation payment (DAP): you pay the total amount yourself.

- A combination of lump sum and rental payments:

A combination of payments is when you combine the two types of payments with meeting your costs. You can split the combination any way you choose.

For example, for an agreed room price of $400,000, you could pay $100,000 as a refundable lump sum and a reduced non-refundable daily payment.

If you choose to pay an amount as a lump sum, the balance is refunded when you leave the aged care home. However, the aged care provider will not refund any amounts drawn down from the lump sum to pay other aged care costs.

Sell investment property and put money into the RAD

You may consider selling the primary residence to pay the bond (RAD). Or maybe you are considering whether it is more beneficial to rent it out to help pay the daily amount (DAP).

You have 28 days after entering aged care to determine how to pay for your accommodation. You are required to pay the DAP until the RAD payment is made:

- if you pay a RAD within those 28 days, you have six months to pay the remaining RAD amount

- if you pay a RAD after those 28 days, it is due as agreed between you and the provider

It would be best to acquire professional financial and legal advice to determine whether leasing or selling your home is more beneficial.

Either way, be aware that what you decide to do with the primary residence may impact the Age Pension assets test.

If you sell the property, its value will contribute towards the Age Pension assets test.

In the event that you lease out the home, its value may contribute towards the Age Pension assets test, depending on when you transitioned into aged care.

If you keep the primary residence without leasing it out, it is absolved from the Age Pension assets test for two years following your transition into aged care. It may vary if you are, or were, a couple when you moved into aged care.

Speak to a Services Australia Financial Information Service (FIS) officer for more information.

Redeem the account-based pension

An account-based pension provides regular, flexible, and tax-effective income via your superannuation.

You can get one when you reach 55 to 60 years of age. It lasts if the money is in your superannuation. However, it is not a guaranteed income for life.

Typically, you get to choose:

- how much do you wish to transfer to the ‘pension phase’ (per the balance transfer cap)

- the amount and frequency of your payments (per the minimum or maximum allowed)

- how you want your super invested (through your fund)

Aged care residents typically pay for accommodation and basic living expenses ($50.16 per day). Residents are also asked to contribute towards the cost of care per their affordability, as measured by the means-test amount (MTA) calculation. This complex formula combines a portion of assessable assets and income to determine a daily affordability amount.

Most people will have money in a self-managed super fund or other superannuation funds, included in the MTA calculation. The assessment rules rely on the person’s age and the form the savings are held. The same rules apply when determining age pension (or other means-tested) entitlements.

These assessment rules create some strategic opportunities that may help reduce the cost of care or increase age pension entitlements.

There are options to transfer money from an assessable investment into an exempt investment, but you should review the whole financial circumstances to check whether the outcome is beneficial.

Income tested and Means-tested fee caps

Calculating how much you will pay is crucial when deciding what aged care services are suitable for you. Some of the fees and costs depend on your financial situation. The Australian Government utilises income assessments or means (income + assets) assessments to determine this.

- When applying for a Home Care Package, you may pay an income-tested care fee. An income assessment dictates if you need to pay this fee.

- If you’re transitioning into an aged care home, you may pay a means-tested care fee and accommodation costs. A means assessment ascertains whether you must pay the means-tested care fee and whether the Australian Government will assist with accommodation costs. In addition, everyone who transitions into an aged care home negotiates a room price before moving in. The means assessment determines if you will have to pay the agreed room price.

Annual and lifetime caps apply to the income-tested care fee for Home Care Packages. Once the caps are reached, you cannot be asked to pay any more, and the Government will cover the fees.

Two annual caps may be applicable regarding home care (at a daily rate):

- If your earnings are equivalent to a part pensioner ($54,990.00 and below), your fee caps at $5,758.45 a year or $15.81 per day (as of September 2021)

- If your earnings are equivalent to a self-funded retiree (more than $54,990.00), your fee is capped at $11,516.92 a year or $31.63 per day (as of September 2021)

The maximum income-tested care fee you may be required to pay over your lifetime is $69,101.75 (September 2021). Any means-tested care fees you pay in residential care will also be counted towards the lifetime cap.

Whether to complete an SA457

The Means Test form (Centrelink form number SA457) needed for residential aged care is not compulsory. However, if the form is not completed, you are classified as “Means not assessed”. There is a resulting risk that you will be charged more Means-Tested Fee than you should be.

In most cases, those with substantial assets will not need to complete the form. But they are still at risk of paying more in the Means-Tested Fee than necessary. They will pay more if their Aged Care Funding Instrument (ACFI) assessment is lower than the Means-Tested Fee.

If the person entering aged care is a supported resident, they must complete the form. Otherwise, they would be categorised as an unsupported resident and therefore required to pay the accommodation payment in full.

If you don’t complete the Means-Tested Form, you will receive at minimum two reminders of its incompletion. Even if the form has been completed and sent in, some people still receive reminders, which means that Centrelink has never received the form or lost it.

Another trap to be conscious of is that the form must be completed given your financial situation when you fill in the form (i.e. as at the “relevant date”. However, the final relevant date is the date you become permanent. Therefore, if your situation has changed between these two dates, the outcome could differ.

Whether to fill out the form may be influenced by how complex and time-consuming it is, mainly if you are involved with private trusts or companies. But before deciding, it is always wise to seek legal and financial advice from a professional experienced and qualified in aged care advice. Look for a lawyer and financial advisor who is accredited aged care professional or holds the Financial Planning Association’s Aged Care Specialist designation.

Whether Home Care Packages are worthwhile for HNW clients

Each home care package has an assigned budget to spend on care services. However, the aged care service will use a part to pay the administration fees. A portion of this budget comes from government subsidies and is partially paid by the person who receives the care.

While a home care package can help make home care affordable, the issue is that the wait can be long, as the number of available packages is limited.

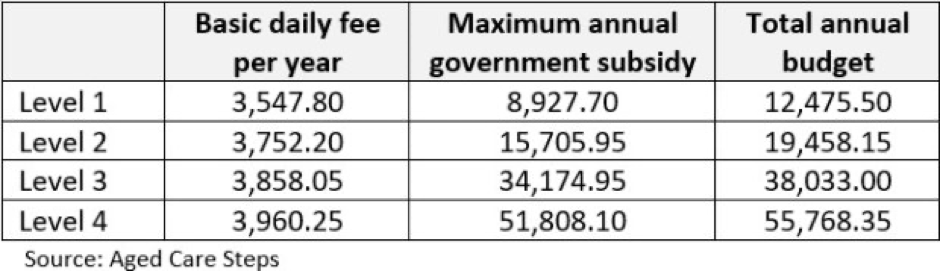

There are four levels of the Home Care Package, with Level 1 providing the lowest amount of care and funding and Level 4 the highest amount.

Home Care Package funds are not paid directly to you, they are distributed to your provider monthly.

Your chosen provider can access these funds to pay for the hours of care, support and administration and advice they give you.

But are you too wealthy to be eligible for government subsidies? Eligibility for an age pension cuts when you have assets or income over certain thresholds.

Unfortunately, home care packages are not the same.

There is no income cap for eligibility to the government subsidies. Alternatively, there is just a cap on the amount payable by the person. The maximum income-tested yearly fee is $11,335.48 (plus the basic fee). Everyone is eligible for government subsidies, except possible people with very high incomes who receive a Level 1 package.

High net wealth clients and aged care – considering super, income streams and downsizer contributions

Once you reach your sixties and are an empty nester, you may want to downsize or find a more appropriate home.

For some retirees, selling the family home can be an efficient way to release some of the equity they have accumulated and make an extra contribution to their superannuation account.

Under the downsizer contribution regulations, your eligible contributions are exempt from some of the normal limits and rules so that you can give your super a meaningful last-minute boost.

It’s also worth remembering that your investment earnings are tax-free when these contributions transition into retirement and start drawing an income. However, if you were to invest the sale proceeds outside super, you would be liable for tax on any income from the investments.

Vogue Advisory Group – helping high net wealth clients transition to aged care

When it comes to financing aged care, it is vital to have a plan that contemplates how to pay for the accommodation and ongoing cost. As well as any cash flow, tax, pension, and estate planning ramifications.

It certainly benefits to seek specialist advice in a highly complex area. However, it can be overwhelming navigating all the options available for your transition to aged care and knowing what is suitable for you. There is a lot to consider! Therefore, it is essential to discuss your preferences and needs and prepare for the future if you can.

Don’t hesitate to contact us if you need financial advice regarding transition into aged care.