Conducting a financial year review, focusing on brief economic and financial markets, is essential.

The 2021/22 financial year review: Key market and macroeconomic development

| Jul 2021 | Global central banks started talking about reducing their QE programmes, given the economic data had been improving faster than they had expected. As a result, gold rallied, and the AUD fell to its lowest since early December 2020. |

| Aug 2021 | Covid-19 continued to spread worldwide, leading to further slowing economic activity, disruptions to global supply chains, and pockets of inflationary pressures. However, the Reserve Bank of Australia (RBA) claimed it would not increase the cash rate until inflation is sustainably within the 2-3% target range and that it did not expect this to happen before 2024. |

| Sep 2021 | The Federal Reserve announced its tapering programme would begin around the end of the year. As a result, iron ore, Australia’s largest export, crashed by -25%. |

| Oct 2021 | Global inflation increased noticeably and rapidly in the US (5.4% year on year) and Australia (3.0%). However, while currently higher than expected, the RBA claimed that inflation is unlikely to stay high. Bond market returns continue to fall as yields rise in response to a growing expectation that central banks would bring forward their timetables for raising rates. |

| Nov 2021 | A new Covid-19 variant (Omicron) reached Australia’s shores. The volatility index shot higher as market fears took hold, resulting in intense selling pressure for risky assets in the month’s final days. The Australian Dollar fell from 75c to 71c, reflecting soft commodity prices, widening interest rate differentials and a general preference for safe-haven currencies during this recent bout of volatility. Federal Reserve Chair Jerome Powell indicated that higher inflation is likely to persist for longer than the Fed initially thought. |

| Dec 2021 | Global and US equities enjoyed an outstanding calendar year. Australian equities posted a solid +17.7% total return, including dividends but underperformed global equities. Rising inflation and bond yields saw Global and Australian bonds post their worst annual return in decades, falling -1.5% and -2.9%, respectively. |

| Jan 2022 | It was a poor start to the new year for financial markets, with all significant financial assets posting negative returns. The US Federal Reserve announced that tighter monetary policy (higher cash rates) is just around the corner. Global bond markets responded to the Federal Reserve’s more ‘aggressive’ tone by rapidly selling bonds, which caused prices to fall heavily and bond yields to rise. As a result, the Australian share market was down (-6.6%) in January, in what was one of the worst starts to a year in decades. |

| Feb 2022 | Russia invaded Ukraine in late February. Concerns emerge that the main threat to the global economy may come in the form of an energy crisis (and higher inflation) which would hit Europe hardest given that Russia currently supplies 30% of Europe’s gas and oil. With US inflation sitting at 7.5% (the highest reading in 40 years) and a very tight labour market, the Federal Reserve signals it will soon be appropriate to raise the target range for the federal funds rate. Australia posts some encouraging economic figures. The unemployment rate comes in at a 14-year low of 4.2%. |

| Mar 2022 | The US Federal Reserve lifted rates by 0.25%, noting that whilst US economic activity and employment continued to strengthen, inflation remained elevated and is likely to persist if there is no action to control it. The RBA kept the cash rate unchanged at 0.10% but hinted that it was warming the idea of lifting rates. As a result, global bond yields spike higher. |

| Apr 2022 | Australia’s headline inflation rate rose to 5.1%. The RBA lifted the official cash rate from 0.25% to 0.35%, the first cash rate increase in over a decade. The US Federal Reserve delivered its most significant interest rate increase since 2000. Major global financial assets pulled back sharply on fears that the risk of global stagflation (slow economic growth coinciding with stubbornly high inflation) started to rise. The price of iron ore took a tumble, falling almost -9%, reflecting a marked fall in steel production in China. |

| May 2022 | Financial markets responded to the uncertain economic outlook by posting mixed and volatile monthly results. The oil price continued its sustained rally. In addition, the US recorded a softer inflation reading, giving markets reason to think that the Fed may hit the pause button on tightening too hard and too fast, especially if inflation levels continued to moderate as they expected. |

| Jun 2022 | Nearly all major global markets finished the month exceptionally poorly. The All Ordinaries was down a sobering -9.4%. The MSCI World Index (USD) and S&P 500 were down -8.6% and -8.3% respectively. Global High Yield Bonds crashed a staggering -7.4%. The US hiked a further 75 bps and remarked that the battle against inflation is ‘unconditional’ even if it comes at the expense of jobs (and a recession). |

Financial year review

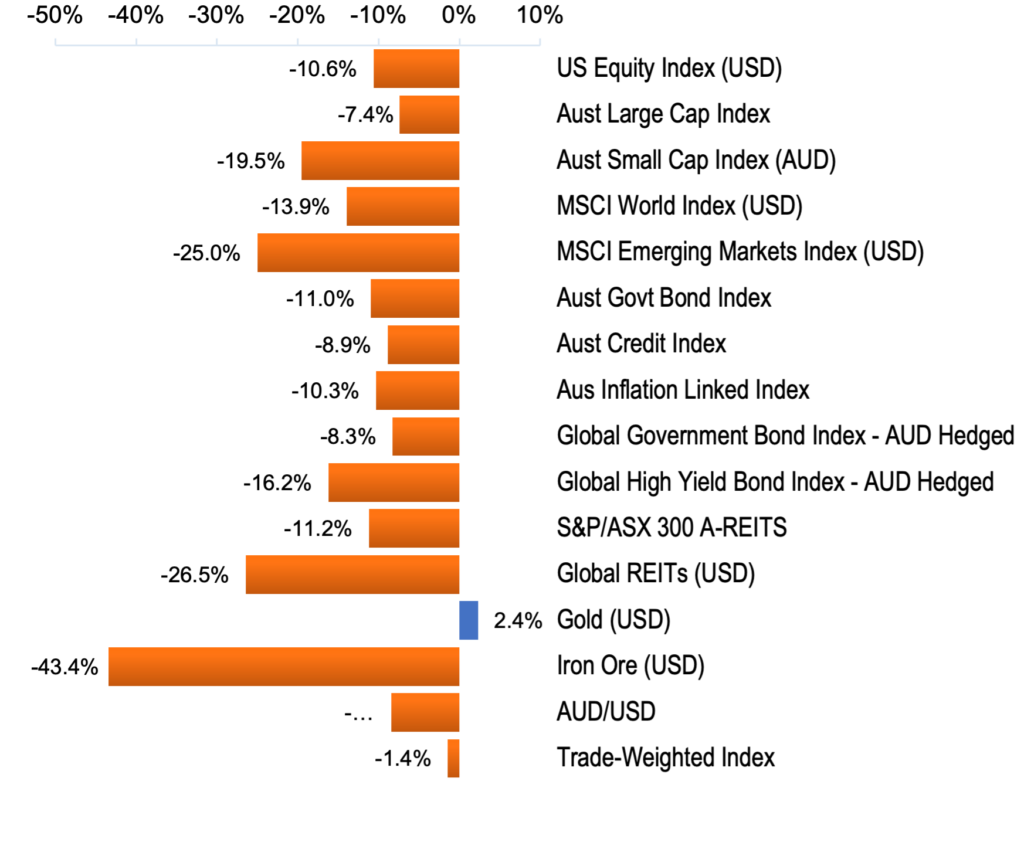

As the calendar of events and the return chart suggests, it was an extraordinary 12 months from both an economic and financial market perspective. However, whilst the 6-month period ending the calendar year 2021 showed positive signs, the second half of the financial year 2021/22 was arguably one of the worst periods we have experienced in many years for investors.

The first half of the financial year was far more encouraging, with solid investment returns to match, as the global economy continued to recover on the steam of ultra-low interest rates, healthy vaccine adoption and a general easing of lockdown conditions. There was a general feeling that the worst of the pandemic was behind us, and a new normal was ahead. General confidence and sentiment were holding up, and consumer demand was strong. Labour markets were improving.

Alas, inflation in the US spiked to 8.6% and 5.1% in Australia, exacerbated by continued COVID-19 supply disruption and the ongoing war in Ukraine. Global financial markets, especially bond markets, responded in a volatile fashion, struggling to come to grips with the implications for financial markets in the face of high inflation, higher interest rates and weaker growth prospects. To put this into context, inflation, when running at a desired 2-3%, is typically considered a welcome development as a modest amount can help drive economic growth. However, the high inflation of the order we are currently experiencing is cause for concern, as it reduces the purchasing power of people’s incomes and devalues people’s savings.

There was nowhere to hide in FY 2021/22. But unfortunately, markets did not discriminate, with bonds, equities, and almost everything falling heavily.

Looking Ahead:

Looking ahead, we contend that financial markets will continue to wax and wane until inflation comes back under control and reverts to target. A potential risk is that central banks may have to commit to higher interest rates if inflation persists at high levels. With inflation at 40-year highs, central banks everywhere are rushing to raise rates even in the face of slowing growth. Both the Federal Reserve and the RBA are on the public record that they are committed to reducing inflation and doing whatever it takes, even at the expense of economic growth.

The financial year 2021/22 ended with significant risk aversion and volatility. However, provided inflation starts to come off the boil as we expect to be the case, the year ahead could shape up to be a better one for investors as central banks rein in their planned monetary tightening.

Vogue Advisory Group – we are here to help you understand the financial market’s past, present, and future.

If you require any financial advice, please get in touch with us, and one of our financial advisors can assist you.